Electric Two-Wheelers In India

Brainwaves Into A Complex World

Earlier this month, Ola announced the “Ola Air Pro” - the world’s first electric flying car.

With a top speed of 350 km/h, Zero CO2 emissions, infinite range, and being 100% electric, it seemed too good to be true.

Unfortunately, it was. It was an April’s Fools Joke! While electric flying cars might not be in our immediate future, electric vehicles definitely are. Especially electric two-wheelers - we’re already seeing usage increase exponentially in India.

In this week, our guest contributor, Prathamesh explores in depth the electric two-wheeler market in India. We also discuss DeFi, “real” coding, the future of food, and more!

Let’s dive in!

Electric Two-Wheelers: The Future?

Written by Prathamesh Dahake

100! A number long ubiquitous with cricketing legend Sachin Tendulkar grabbed eyeballs recently, albeit for quite an undesirable reason. On 17th Feb, petrol prices crossed the Rs. 100 mark leaving everyone in a tight spot in an already pandemic-hit life. According to a recent survey conducted by the Mint, 51% of citizens are cutting spending to cope with high fuel prices, with 21% cutting spending on essentials. TERI anticipates that prices of petrol and diesel would remain at high levels and will continue to increase in the long-term.

Given this context, could this act as a catalyst for the growth of electric vehicles? More specifically, given that a majority of the vehicles on the road are two-wheelers, can this lead to an increase in electric two-wheelers?

We decided to take a deep dive into the Electric 2-Wheeler (E2W) in India.

Indian E2W Ecosystem

The E2W market in India has grown significantly at a CAGR of 62% from FY16 to FY20. In FY20, E2W sales stood at 152,000 units and accounted for ~97.5% of all the EVs sold in India. Moving forward, the market is expected to grow from 1.52 lakh units in FY20 to ~34.5 lakh units by FY25 at a CAGR of 87%.

Significant disruption is anticipated in the E2W space post-2024, due to the expected fall of battery prices below $100kWh. This price is seen as the point around which EVs will start to reach price parity with internal combustion engine (ICE) vehicles. As per estimates, from FY22 onwards, with every 7-8% YoY fall in battery prices, the share of E2Ws in total 2W sales is projected to double, and the E2W penetration is predicted to increase from 0.9% in FY20 to 7-10% by FY25.

Market Segmentation

The E2W market can be segmented as per 3 different speed categories -

In FY20, low-speed scooters constituted a whopping 90% of all the E2Ws sold in India. These scooters have been able to gain such traction primarily due to their low cost - at around Rs.30,000 – Rs.50,000, and also due to the lack of need for RTO registration and driver’s licence or helmets. But in the long-term, EV manufacturers are banking on high-speed scooters to grab a bigger share of the pie. This is because, under the new FAME 2 guidelines, only high-speed E2Ws are eligible for incentives.

The high-speed E2Ws offer is the only category that offers efficiency and performance that is near-equal or better than their ICE counterparts. However, between FY18-FY20, about 14 new models with speed under 25kmph, and 20 new models with a top speed in the range of 40-147kmph were launched. The market did not witness any new entrants within the 25-40kmph segment.

The following market map shows the different E2W models available in India -

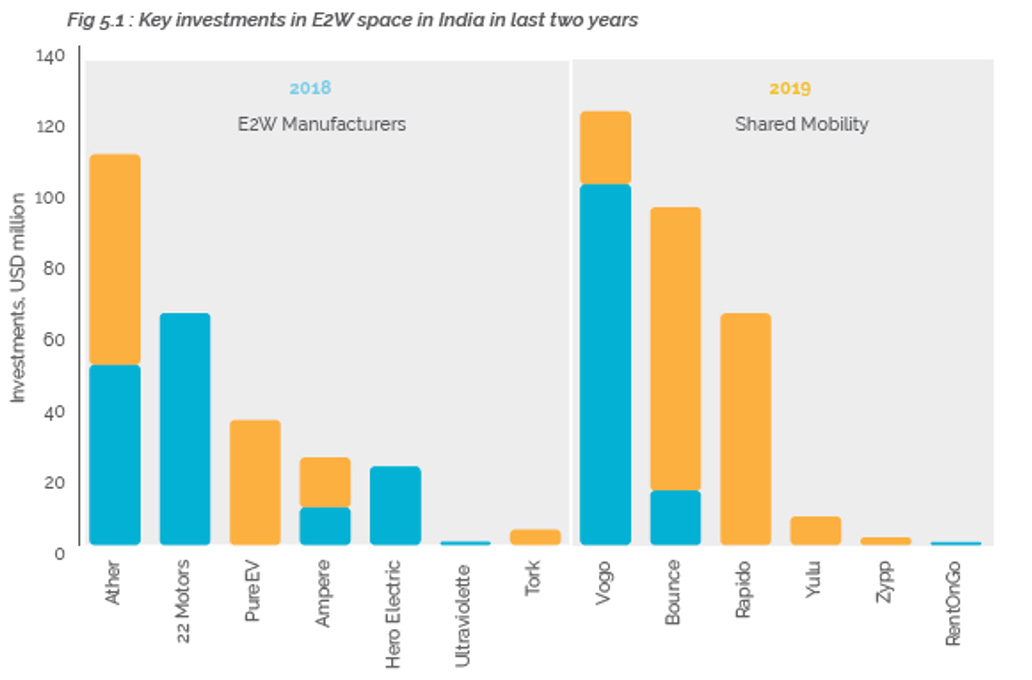

Investment Scenario

In 2018-19, more than $600 million was raised by E2W companies in India. Not just startups, even legacy brands like TVS, Bajaj and Hero have entered the E2W market and have started their own line of electric vehicles.

Ola is betting big on E2Ws too. In May-2020, it acquired Etergo, an innovative electric scooter OEM based out of Amsterdam, and announced its entry into the premium E2W market, both globally and nationally. In Dec-2020, with tremendous news coverage, it announced an Rs. 2,400 crore ($340m) investment plan to set up the “world’s largest e-scooter manufacturing plant” in Hosur, Tamil Nadu.

These investments have helped startups and manufacturers overcome the issue of large upfront capital required for the plant setup and have also contributed towards keeping the prices of E2Ws affordable while boosting R&D efforts. Comparing the investments, we can infer that investments are skewed towards shared services than private vehicles since the cost economics work better in the shared mobility segment.

Why Target the 2-Wheeler Segment?

1. Market Opportunity:

India is currently the 4th largest auto market in the world and is expected to displace Japan as the 3rd largest auto market by 2021.

In FY20, 21.6m automobiles were sold in India and the sector was dominated by the 2 wheelers segment (81% of the market with ~17.5m 2Ws sold). 2-wheeler sales in India are expected to grow at a CAGR of 4% from FY21-FY25, which translates into a whopping ~21.3m 2Ws sold domestically by 2025! Even though the segment was hit hard during the pandemic, this segment is expected to make a strong come back, especially in the short term as people would opt for the cheapest and fuel-efficient mode of personal transport.

2. Fuel Consumption & Pollution Concerns

India is amongst the top 3 crude oil importing (by $ value) countries in the world, and its dependence on crude imports has been increasing over the years. Such over-reliance on fossil fuel imports not only leaves end customers susceptible to volatile fuel prices but also adds to pollution woes, and the 2W segment lies at the heart of all these problems.

2Ws account for over 62% of all petrol consumption in India as compared to 27% by 4Ws and 6% by 3Ws. In major Indian cities, two-thirds of the pollution load is due to 2Ws. They are responsible for 30% of the particulate matter load, 10% points more than the contribution from cars. All these facts answer our question as to why 2Ws need to be at the centre of electrification, and E2Ws provide us with an opportunity of killing two birds with one stone.

3. Penetration & Propensity to Transition

As of FY20, EVs represented <1% of the overall auto market, with E2Ws having a measly 0.9% penetration. Fast forward, the Indian EV market is expected to be dominated by light electric mobility vehicles i.e., the 2Ws and 3Ws. KPMG expects 25-35% E2W, and 65-75% E3W penetration by 2030. Going by the forecasts, we can surely say that E3Ws would be the fastest-growing segment, but in absolute terms/numbers, the E2W market would still have very high upside potential and would at least be 10x bigger in comparison to the E3W market. On the contrary, the penetration trajectory for 4W passenger vehicles (PV) and commercial vehicles is expected to be one of the laggards, with just 10-15% penetration in the personal segment and 20-30% penetration in the commercial one by 2030.

Now that we have more context regarding the current and future market penetration levels for different EV segments, let us try to understand the major challenges influencing the EV purchasing decision -

High Upfront Costs

According to a survey conducted by TERI, more than 70% of people are aware of the fact that operational costs associated with EVs are less than that of ICE vehicles, yet EVs have a poor adoption rate owing to their high upfront cost. Indian consumers are highly price-sensitive, and the high upfront cost happens to be the topmost deterrent in EV adoption. This high upfront cost can be attributed to the battery which constitutes about 40-50% of the EV cost, and as the vehicle size increases the battery costs associated with it increases non-linearly.

Going by the same logic one would expect that E2Ws would have the lowest upfront premiums when compared to E3Ws and E4Ws, but the reality is somewhat distorted. E2Ws do have one of the lowest upfront premiums, and on average, they trade at ~1.0-1.5x their ICE counterparts, but they also compete very closely with E3Ws. E3Ws also trade at comparable costs, 0.9 – 1.5x their ICE counterparts, mostly due to the presence of a plethora of recognized brands and products which have brought down the upfront prices, plus the majority of the E3W vehicles run on Lead Acid batteries which are much cheaper than the Li-on batteries used in E2Ws. Therefore, from an upfront cost perspective we can say that both E2Ws and E3Ws have a high transition propensity, whereas E4Ws are still very expensive (40-60% premium) making them an unpopular mode of transport to own.

Range Anxiety

Another significant concern for people looking to buy an EV is range anxiety or in layman terms, people are not sure how far their EV will run on a single charge. Just compare the scenarios of buying an ICE vehicle vs. an EV - while purchasing an ICE vehicle we are fully aware of its mileage (which at times is more or less very accurate) and even after years of usage the mileage does not drop as much. However, the same cannot be said for EVs, mostly because the metric – distance per one full charge is not very static/reliable. For starters, batteries lose performance more quickly as they get older or when subjected to improper charging/discharging cycles. They tend to underperform in extreme temperatures and cannot be relied upon in demanding situations like traversing through tough terrains or while carrying loads or even people way above the safety limits, which happens a lot in India. Additionally, there is the problem of vampire drain, which means that the battery will slowly lose its charging when left in an idle condition. To highlight the severity of vampire drain, Tesla even has a page dedicated to it.

“Your Tesla loses range when parked caused by Vampire battery drain. This can vary from a few miles per day to quite significant amounts depending on the settings in the car and can be a problem if leaving your car while on holiday”

The problem of range anxiety would drastically reduce if enough public charging stations and battery swapping centres/kiosks were to be installed. Looking at the current status, it can be said with fair confidence that it would take at least another 4-5 years before EV charging stations become commonplace sighting. In the absence of charging stations, another way around reducing range anxiety could be - route predictability. It basically means deploying EVs to use cases where the destination or the distance travelled roughly remains the same on a daily basis. Higher route predictability is one of the major reasons why E2Ws and E3Ws are expected to have better adoption rates when compared to E4Ws. Daily office commute and visits to fixed marketplaces are examples of highly predictable routes where E2Ws tend to find huge traction.

On average, Indians tend to make short-distance trips (<10km) at least five days a week but the medium (up to 100km) and long-distance (>100km) trips are rare. This ability of E2Ws to cover short distances easily has impacted consumer buying behaviour and has worked in its favour.

Another space that offers high route predictability and a huge opportunity for E2Ws is hyperlocal delivery. In the hyperlocal delivery model, vehicles are deployed for deliveries from the stores serving their customers within a 10-12km radius, hence the issue of vehicle range gets eliminated. The bikes then return to the central hub for recharging after their delivery slot is over. The delivery slot spans ~2 hours which falls well within the stipulated run-time for E2Ws. This lowered range anxiety plus added operational cost benefits is pushing vendors like BigBasket to go the EV way. In fact, BigBasket has already planned to ramp its fleet of 800 EVs to 4,000-5,000 EVs by 2023.

The last-mile segment, dominated by intracity travel, offers highly predictable routes for E3Ws. Autos and E-ricks have always served as primary modes of transportation for lakhs of students and working professionals across the country and will continue doing so. E-commerce delivery could be another big opportunity which not only caters to fixed delivery destinations but also provides scheduling of routes in advance. Local civic bodies could deploy E3Ws for applications such as waste management and chemical fogging purposes.

However, the case for E4Ws is a bit different. People generally use a 4W for outdoor purposes, which involves long drives. Here not only do E4Ws fall short of range but also of charging infrastructure at remote places. At times, the roads are not maintained which increase the total drive duration, thereby adding to the overall range anxiety surrounding the EV.

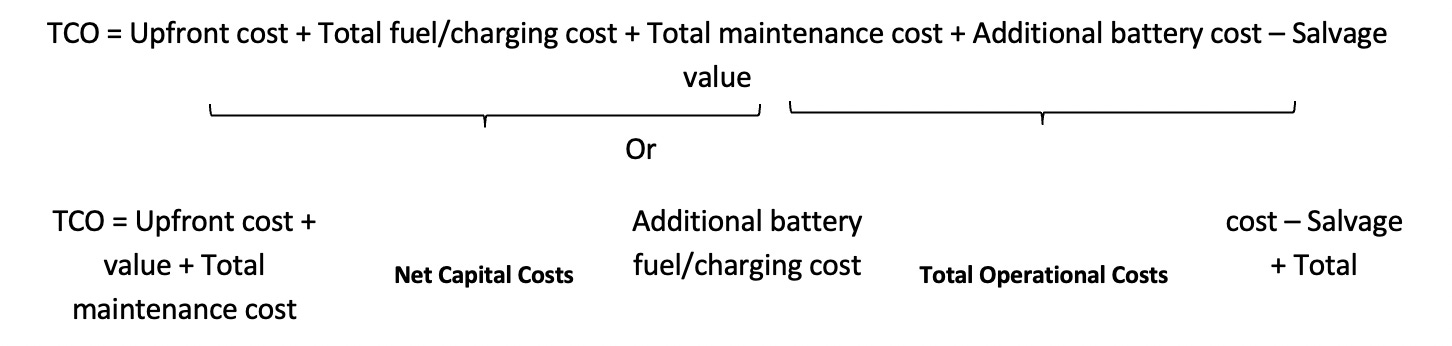

Total Cost of Ownership (TCO)

High upfront cost is a key barrier to EV adoption, but it falls short of being a key metric while performing an apples-to-apples comparison with ICE vehicles. Rather, TCO is a more accurate assessment of the economic efficiency of EVs vis-à-vis ICE vehicles. TCO can be defined as the sum of all costs involved in the purchase, operation and maintenance of a given asset during its lifetime. From an EV perspective,

EVs are able to achieve TCO parity with ICE vehicles owing to lower operating costs, which depend on the daily utilization levels and the vehicle holding period. As the utilization levels increase i.e., for every extra km driven, TCO per km for EVs shows a greater reduction in comparison to ICE vehicles. This translates into greater savings for EV users due to lowered fuel and maintenance costs - even after accounting for battery replacement costs.

a) Low-speed and medium-speed E2Ws are already at parity with ICE vehicles with less than 10km of daily usage. The TCO for high-speed E2Ws is not yet attractive and is achieved at 40km+ daily usage.

b) E3Ws have substantially less (~17%) TCO than ICE vehicles for average daily usage of 100km.

c) Within 4Ws, retail-medium and commercial vehicles are very close to achieving parity with ICE 4Ws. Commercial E4Ws are expected to reach parity much faster, given greater adoption and utilization by fleet operators. However, in the premium category, there is still a wide gap between the TCO for EV and ICE vehicle. This can be attributed to the huge upfront premium one has to pay while buying a premium E4W.

Parting Thoughts

Both E2Ws and E3Ws offer a promising solution to India’s pollution and fuel price woes while addressing two different modes of transportation - shared and private. The EV market is highly under-penetrated and is expected to boom in the future, but that hinges on the development of an end-to-end competitive ecosystem consisting of EV manufacturers, charging infrastructure and maintenance services providers, and the establishment of a robust second-hand marketplace. Added incentives on the part of both government and EV manufacturers would surely accelerate EV adoption in India.

In addition to the government subsidy on EVs, recurring, non-financial incentives such as toll fee or congestion fee waivers, reserved parking spaces and exclusives drive lanes could drive preferences in favour of EVs. Norway has been highly successful in complementing financial incentives with non-financial incentives. As a result, it was able to increase its EV penetration rate from 1% in 2010 to 54% in 2021 - one of the highest in the world!

What We're Watching

‘Decentralized Finance’ (aka DeFi) seems to be slowly finding itself in the daily lexicon of people. But what does it really mean?

In this episode of ‘Forbes Defined’ Alexander Pack, a venture capitalist focused on the cryptocurrency space, explains why DeFi has the potential to reshape many of the financial services we use every day.

Thought Leaders Speak

The rise of no-code has led to a lot of “real coders” getting protective about what qualifies as “coding” and what doesn’t. The author of ‘Real’ Programming Is an Elitist Myth believes “coding” needs a wider definition. What do you think?

Tweet of the Week

What We’re Listening To

In this episode of “The Investors’ Podcast” investor and philanthropist, Jim Mellon discusses his new book, “Moo’s Law". The book is about the future of food and how investors, can profit.

CNBC has referred to Jim as “Britain’s answer to Warren Buffett” and he brings a wealth of knowledge to this very wide-ranging discussion.

That's all for this edition! We hope you liked it and would love to get any feedback you may have. This newsletter is written and curated by Mishaal Nathani and Ashutosh Gehlot.

Enjoyed this newsletter?

Get The Skeptic Investor in your inbox every Sunday. Click below to Subscribe:

Feel free to reach out if you have any suggestions or you’d like to contribute to the TSI:

Disclaimer: This content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Nothing contained in the newsletter constitutes a solicitation, recommendation, endorsement, or offer by us or any third party service provider to buy or sell any securities or other financial instruments in this or in any other jurisdiction in which such solicitation or offer would be unlawful under the securities laws of such jurisdiction.

Nice research and well connected to links for references.But the language seems to be little high , good for subject experts but drives non-subject people who are unaware of the industry (like me 🙂) to the dictionary 😄😁. please think about this issue in your next edition

Very well researched article giving holistic picture of where we are now on EV and what does future hold for EVs in India!